Sea Change 2.5

The Supply-Side Reckoning: an exercise in thinking about the future

In December 2022, Howard Marks published a memo titled Sea Change. In it, he argued that the investment world was undergoing one of those rare, fundamental shifts—a transformation so deep that the strategies which worked for the prior four decades would not be the ones that worked going forward. He had witnessed only two such shifts in his fifty-three years in the business. The first was the birth of risk/return thinking in the late 1970s, when investors stopped avoiding risk altogether and began pricing it instead. The second was the long decline in interest rates that began after Paul Volcker broke the back of inflation in the early 1980s—a tailwind that carried every category of financial asset upward for forty uninterrupted years.

The third sea change, Marks argued, was the reversal of that tailwind. After four decades of declining rates, the environment had shifted: inflation was back, the Federal Reserve was tightening aggressively, and the cost of capital was rising. The moving walkway that had carried investors effortlessly forward had stopped. Worse, it might be running in the other direction.

The core thesis was elegant and correct. But it was also, primarily, a monetary story. The mechanism Marks identified was straightforward: loose monetary policy had suppressed the cost of capital for decades, inflating asset prices across the board. Now that monetary policy was tightening, those dynamics would reverse. Interest rates would normalize in the 2–4% range, prospective returns would be higher but so would the hurdle, and the era of easy money was over.

Three years later, I want to revisit this thesis—not because it was wrong, but because I believe we are approaching a second, potentially more powerful phase of the same sea change. One that is not primarily monetary in nature, but physical.

The Thesis on Hold

It is worth acknowledging what has happened since Marks wrote his memo. The recession that seemed all but certain in 2023 never materialized. The stock market, rather than continuing its decline, staged one of the most aggressive rallies in recent memory. The S&P 500 did not just recover its 2022 losses—it surged to new all-time highs, driven by a mix of an improving economy, increasing profits and gross margins and increasingly, a narrow cohort of technology companies riding the artificial intelligence narrative. The Fed did eventually pause its rate hikes, and while it has not returned to the zero-rate regime, interest rates have settled into roughly the 2–4% band that Marks predicted would be the new normal.

On the surface, this might look like the sea change was overblown. Markets adapted. The economy proved resilient. Investors who bought the dip in late 2022 were handsomely rewarded. But this reading confuses a pause with a resolution. The underlying structural forces Marks identified have not gone away—they have merely been temporarily offset by the extraordinary enthusiasm surrounding AI. And crucially, the very thing generating that enthusiasm is now creating a new set of inflationary pressures that may prove far more persistent than the monetary ones.

Sea changes, as Marks himself noted, unfold over decades. The original story is not finished. But I believe we may be entering a pivotal new chapter.

The Second Engine: Supply-Side Pressure

The original sea change thesis was primarily a demand-side story told through monetary policy. Too much money chasing too few goods, fueled by decades of easy credit and quantitative easing. The policy response—raising rates—was designed to reduce demand and bring the system back into balance.

What I want to draw attention to is a parallel development that is less discussed but potentially more consequential: a structural increase in the cost of supply.

Several enormous physical build-outs and demographic trends are converging simultaneously. The first is the AI infrastructure boom. The second is the reshoring of manufacturing supply chains, driven by geopolitical fragmentation and national security considerations. The third is the decreasing supply of marginal labor due to an aging population, reshoring and immigration limitations. Together these all require massive capital expenditure, raw materials, energy, labor, and land. And they’re all happening at the same time.

The AI build-out alone is staggering in scale. Capital expenditures across the major hyperscalers—Microsoft, Google, Amazon, and Meta—are at historically unprecedented levels in 2026. These companies are racing to build data centers not because they have clear visibility into the returns, but because falling behind in AI compute capacity is perceived as existential. The game-theoretic dynamics are brutal: even if you suspect overinvestment, the cost of underinvestment—losing out on the future AI driven revenue—is considered far worse.

Figure 1: Hyperscaler Capital Expenditures (2020-2026E)

But data centers do not run on optimism. They run on electricity, semiconductors, copper, concrete, water, and memory chips. Each of these inputs is seeing its own supply-demand imbalance. The demand for high-bandwidth memory is outstripping supply, with structural consequences for everything from server costs to consumer electronics pricing. The demand for electricity to power AI workloads is straining power grids that were not designed for this load. And the demand for construction labor, already tight from reshoring initiatives, is being further intensified.

Figure 2: US Construction Labor Market Tightness

Figure 3: High-Bandwidth Memory (HBM) Supply Constraints

Layer on top of this the reshoring trend. Decades of globalization gave the developed world a powerful deflationary force: cheap manufactured goods and cheap labor sourced in low-cost countries. Marks noted in his original memo that consumer durables prices fell roughly 40% between 1995 and 2020, shaving an estimated 0.6 percentage points off annual inflation. That era is over. The move to diversify supply chains away from China, driven by tariffs, geopolitical risk, and national security mandates, means building new factories in higher-cost locations. This is the right strategic decision for a nation, but it is not a cheap one. To add to this trend, demographics and the makeup of the global workforce has completely changed, for the worse (as shown in ‘The Great Demographic Reversal’ by Charles Goodhart and Manoj Pradhan). All these trends point towards more expensive local labor and supply constraints.

Figure 4: Copper Prices — Supply Constraint Indicator (2020-2026)

The net effect is a supply-side cost shock that operates independently of monetary policy. You could cut interest rates to zero tomorrow and it would not create more copper, more electricity, or more high-bandwidth memory. The constraints are physical, not financial.

Energy: The Connective Tissue

Of all the supply-side pressures, energy is the most important, because energy inflation permeates everything.

Consider the chain of causation. AI requires enormous amounts of electricity. Meeting that demand, in many cases, means running existing energy plants harder and longer than planned, while simultaneously building new capacity. It’s unfortunate that the green energy push has limited out access to nuclear energy. Instead, the increased demand for electricity raises the demand for natural gas, coal, and eventually oil, because the grid cannot transition to renewables fast enough to meet the pace of AI deployment.

Figure 4: US Data Center Electricity Demand Projections

Higher energy costs feed directly into the cost of producing and transporting every physical good in the economy. Gasoline costs more. Freight costs more. Manufacturing costs more.

This is not the transitory, demand-pull inflation of 2021–2022, where too much stimulus money chased too few goods during a pandemic reopening. This is cost-push inflation driven by a physical reality: we are trying to build massive infrastructure systems simultaneously, while limiting the input sources. Energy, materials, and skilled labor is not infinite, and we’ve been pushing these offshore for 40 years.

The monetary policy implications are uncomfortable. When inflation is driven by excess demand, the central bank has a clear tool: raise rates, cool demand, let the economy rebalance. But when inflation is driven by structural supply-side costs, raising rates does not solve the underlying problem. It simply increases the cost of capital on top of already rising input costs, compressing margins from both sides. The Fed might find itself in a bind that rhymes, uncomfortably, with the 1970s.

Figure 5: CPI Inflation — Year-over-Year Change (1950-2026)

The Moving Walkway in Reverse

In his original memo, Marks used a memorable metaphor. He compared the four decades of declining interest rates to a moving walkway at an airport. Investors thought their returns came from their own skill—their ability to pick the right stocks, the right funds, the right strategies. In reality, a significant portion of their returns came from the walkway itself: the steady tailwind of declining rates lifting all asset prices.

If declining rates were the moving walkway carrying investors forward, then what we could be about to experience is that walkway gradually reversing direction. And the supply-side pressures I have described are adding a headwind on top of that.

Think about what rising cost of capital does to the investment math. Every business plan, every leveraged buyout, every real estate development, every infrastructure project is built on assumptions about the cost of debt and equity financing. When the cost of capital was declining, the math got easier every year. A deal that looked marginal at 8% financing became attractive at 6%, and spectacular at 4%. The refinancing cycle was a gift that kept giving.

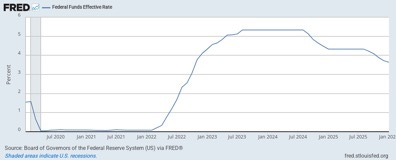

Figure 6: Federal Funds Rate (2020-2026)

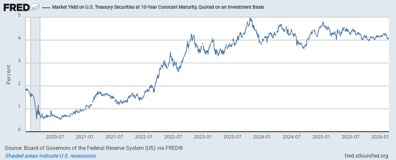

Figure 7: 10-Year Treasury Yield (2020-2026)

Despite the Fed cutting 175 bps since Sep 2024, the 10Y yield rose from ~3.6% to ~4.05%. Is the bond market pricing in structural inflation?

Now reverse that process. A deal financed at 4% that needs to be refinanced at 6% or 7% doesn’t just become less profitable—the fundamental economics may break entirely. The hurdle rate for new investments rises. Capital allocation becomes more disciplined, not because CEOs suddenly discovered virtue, but because the market demands it.

This is already playing out in the AI infrastructure cycle itself. The hyperscalers are spending hundreds of billions on data centers, but their cost of capital is rising. Public market scrutiny of their capital expenditures is intensifying quarter by quarter. And the companies they are building this infrastructure for—the model companies, the AI startups, the enterprises adopting AI—face the same rising cost of capital. None of the major frontier model companies are profitable. As their funding costs rise, they face a stark choice: raise prices to reach profitability, or face capital constraints that slow their growth.

The trajectory leads in one direction: higher prices, higher cost of capital and a recession driven reset.

Implications for Financial Assets

If the cost of capital is structurally rising—driven by both the normalization of interest rates and the physical supply-side pressures I’ve described—then the implications for asset prices are significant.

The most direct effect is on long-duration assets. When the cost of capital rises, the present value of future cash flows declines. Companies valued primarily on the promise of distant profits—growth stocks with high multiples and thin or negative current earnings—face the steepest repricing. Multiples contract. The market’s willingness to pay for a dollar of earnings five or ten years from now diminishes. This is not a commentary on whether those companies are building valuable products; it is simply the mechanical effect of discounting future cash flows at a higher rate.

For capital-intensive businesses, the math is particularly punishing. Companies pouring money into physical infrastructure—data centers, chip fabrication, manufacturing plants—face rising hurdle rates at exactly the moment their input costs are also climbing. The squeeze comes from both sides: the cost of the capital they deploy goes up, and the cost of what they build with that capital also goes up. This dynamic puts enormous pressure on the AI infrastructure cycle, and specifically neo clouds – Coreweave, Nebius and Iren. Even if the demand for AI services proves as robust as the bulls expect, the returns on the capital invested to meet that demand may disappoint.

Conversely, capital-light businesses with large existing cash flows and minimal reinvestment needs are relatively advantaged. When the cost of deploying capital rises, the value of not needing to deploy capital increases. Companies that generate substantial free cash flow from existing operations—without needing to build new data centers or factories to sustain that cash flow—become more attractive on a relative basis.

The Counter-Narrative: Deflation Through Efficiency

There is, however, a substantial counter-narrative to the inflationary case.

The same artificial intelligence that is driving supply-side cost pressures through its infrastructure demands is also, simultaneously, generating enormous efficiency gains across the economy. These efficiency gains are deflationary. And they may, over time, partially or even fully offset the inflationary pressures. Additionally, compute increases dramatically in token per watt efficiency due to both hardware and software improvements.

Consider the range of efficiencies AI is already enabling. Freight and logistics companies can optimize delivery routes, load utilization, and scheduling to move more goods with fewer resources. Retailers can optimize shelf space, inventory management, and demand forecasting to reduce waste. Software companies can build and iterate on products with a fraction of the engineering headcount they previously required. Customer service, legal research, financial analysis, content creation—in each of these domains, AI is enabling the same output with materially fewer human hours.

Transportation efficiency alone offers enormous room for improvement. Better optimization of shared travel, mass transit, freight routing, and last-mile delivery could significantly reduce the cost of moving people and goods. Energy efficiency in data centers themselves is improving rapidly, with each new generation of chips delivering more compute per watt.

The question is one of timing and magnitude. The supply-side cost pressures are happening now, in the physical world, constrained by the speed at which you can build power plants and fabricate memory chips. The efficiency gains are also happening now, but their full economic impact takes longer to materialize, because they require organizational adoption, process redesign, and behavioral change. Enterprises do not become 30% more efficient overnight just because an AI tool is available. The adoption curve is measured in quarters and years, not weeks.

This creates an asymmetry. In the near to medium term, the inflationary pressures from physical build-outs may outrun the deflationary pressures from efficiency gains. The cost of building the AI infrastructure arrives before the full productivity benefits of using it. In the longer term, the efficiency gains may prove to be the more powerful force. But investors live in the near term, and the near term looks inflationary.

The resolution of this tension—between the inflationary cost of building the AI future and the deflationary benefit of living in it—will be the defining economic question of the next decade.

The Flows Problem

There is another force at play that, barring Michael Green, receives insufficient attention in most macroeconomic analysis: the structure of capital flows into financial markets.

Over the past several decades, the combination of declining interest rates and the rise of passive investing has created an enormous, largely automatic flow of capital into equities. When money market funds yield zero and bonds offer negligible returns, the rational default for every saver, every 401(k) participant, every target-date fund is to allocate heavily to stocks. The S&P 500 index fund has become the default savings vehicle for an entire generation.

This dynamic is powerful and self-reinforcing. Inflows into passive equity funds push stock prices higher, which generates positive returns, which attracts more inflows. The “buy the dip” mentality that has characterized the post-2009 market is not only a reflection of investor courage or conviction—it is a mechanical consequence of persistent, automatic inflows into a fixed basket of securities.

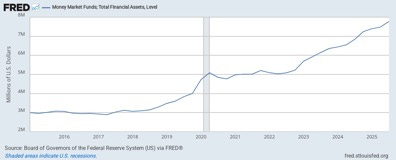

But what happens when interest rates rise and suddenly there are alternatives? When a money market fund yields 4–5%, that calculus begins to change, as we saw over the past two years. What happens if they increase to 7%? The risk premium demanded for holding equities becomes meaningful again, because the risk-free alternative actually pays something. For the first time in over a decade, savers have a real choice.

Now imagine a modest shift in the default allocation. Not a dramatic exodus from equities, but a gradual rebalancing—say, from an 80/20 stock-bond split to a 60/40 or even 50/50 allocation, driven by the simple observation that bonds and money market funds now offer reasonable compensation for their lower risk. The impact on equity market dynamics would be substantial. The constant bid underneath the market—the automatic, price-insensitive buying from passive flows—would weaken.

Figure 8: US Money Market Fund Assets (2015-2026)

The buy-the-dip reflex that has been so reliable for fifteen years depends on the continuous, automatic flow of new money into equity funds. If that flow slows, or if it begins to divide more evenly between equities and fixed income, the market loses a critical support mechanism. Corrections become deeper and longer. Recoveries become less automatic. Multiples shrink. The margin of safety that investors have enjoyed from the sheer force of passive inflows begins to erode.

This is not a prediction of imminent catastrophe. It is an observation that the plumbing of the market—the structural flows that have supported equity valuations for over a decade—could be quietly shifting in a direction that favors fixed income over equities at the margin. And in markets, changes at the margin are what matter most.

The Vulnerability of the Saving Class

There is a final thread that ties the flows argument to the AI disruption thesis, and it is perhaps the most unsettling.

The individuals who contribute the most to passive equity flows are not day traders or institutional allocators. They are white-collar workers earning comfortable salaries—the software engineers, financial analysts, project managers, marketing professionals, and corporate administrators who contribute to their 401(k) every paycheck. These are the people for whom the default S&P 500 allocation in their retirement plan represents their primary exposure to financial markets.

This demographic is precisely the one most exposed to AI-driven labor disruption. Not factory workers, who have already been through decades of automation, or service workers, but knowledge workers—the people who process information, write documents, analyze data, manage projects, and coordinate activities. These are the tasks AI is learning to perform at increasing speed and decreasing cost.

A recession concentrated among white-collar, high-saving-propensity workers would be unusual by historical standards. Most post-war recessions have hit blue-collar and service workers hardest, while the professional class was relatively insulated. But AI-driven displacement could invert that pattern. If the workers most likely to lose their jobs or see their compensation decline are also the workers most responsible for the steady flow of capital into equity markets, the second-order effects on market structure could be significant.

Fewer paychecks mean fewer 401(k) contributions. Reduced compensation means reduced savings. Uncertainty about job security shifts the psychology from long-term investing to short-term preservation. Each of these effects weakens the passive flow mechanism that has supported equity valuations.

None of this is a certainty. It is a scenario whose probability has increased. The pace at which AI tools are capable of performing knowledge work is accelerating faster than most people appreciate. The companies developing these tools are explicit about the goal: to automate as much cognitive labor as possible, as quickly as possible. Whether the labor market adjusts through displacement, wage compression, or a slower process of role redefinition remains to be seen. But the direction is clear, and the population most affected is the same population that has been the engine of passive equity flows.

Putting It Together

Let me attempt to weave these threads into a coherent picture.

Howard Marks argued in 2022 that we were in the early stages of a sea change driven by the end of the declining interest rate era. I believe he was right, and that the thesis has only grown stronger, not weaker, despite the market’s subsequent rally.

What has changed is the composition of the inflationary pressure. The original thesis was primarily monetary: too much stimulus, too much liquidity, rates needing to normalize. That process has largely occurred. Rates are in the 2–4% range. The Fed is no longer at zero.

But a second, more structural engine is now firing. The simultaneous build-out of AI infrastructure, reshored manufacturing, together with demographics, is creating supply-side cost pressures that are physical in nature and cannot be resolved by monetary policy alone. Energy costs, materials costs, and labor costs are rising not because of excess demand stimulus but because we are asking the physical economy to do these enormous things at once.

These supply-side pressures flow through to the cost of capital. When input costs rise, businesses need more capital to achieve the same output. When inflation persists because of structural supply constraints, central banks cannot cut rates to stimulate growth without reigniting price increases. The cost of capital stays elevated, or rises further.

Meanwhile, the structural supports for equity markets weaken. Higher yields on safe assets give investors real alternatives to stocks for the first time in over a decade. And the demographic most responsible for passive equity inflows—white-collar knowledge workers—faces an unprecedented threat from the very technology that is driving the current market enthusiasm.

The counter-narrative is real: AI-driven efficiency gains could, over time, create deflationary forces powerful enough to offset the supply-side pressures. But there is a timing mismatch. The costs are here now. The full benefits take years to materialize. Investors who are pricing the benefits without adequately weighing the costs may be making the same mistake that the Nifty Fifty investors made in the early 1970s: confusing the quality of the underlying trend with the safety of the current price.

What To Do About It

I am not in the business of making macro forecasts, and I am wary of anyone who claims certainty about the direction of interest rates, inflation, or the economy. The world is complex, adaptive, and frequently humbling to those who think they have it figured out.

But I do believe in knowing where we are, even if we cannot know where we are going. And where we are, it seems to me, is in an environment where the probability of it being structurally different from the one that prevailed for most of the last four decades has risen dramatically. The cost of capital is rising, driven by forces that are both monetary and physical. The free lunch of declining rates is over. The supply side of the economy is under pressure from multiple simultaneous infrastructure demands. And the flows that have supported equity valuations are vulnerable to disruption.

None of this means markets will crash tomorrow. Markets can remain expensive for a long time, especially when a powerful narrative—like artificial intelligence—captures the collective imagination. But the margin of safety is thinner than it has been. The tailwinds are weaker. And the range of outcomes is wider.

In Marks’s original memo, he concluded by noting that we had moved from a low-return world to a full-return world—one where credit instruments could finally offer meaningful yields and lenders held better cards than borrowers. I think the next phase of this sea change adds a layer of complexity: we are moving into a world where the returns demanded by capital providers will continue to rise, because the risks embedded in the physical economy—energy constraints, supply chain fragility, infrastructure bottlenecks—are not the kind that can be wished away by a dovish Fed.

The strategies that worked in the era of declining rates and abundant liquidity may not be the ones that work in an era of rising costs and physical constraints. The investors who thrive in this environment will be those who understand that the sea change is no longer just about monetary policy. It is about the physical world reasserting its claim on the financial one.

That is the sea change 2.5 I am talking about.