2024 Wrapped: Hits, Misses and most played

50.5% upside in another amazing year driven by the power of music.

2024 was a significant year for my portfolio and investment journey. First, I beat the market by ~20% with my overall portfolio increasing an amazing 50.5%. More importantly, I felt that my investment process was better, and more at ease (not necessarily confident), but comfortable in my own skin as an investor. During 2024 I managed to focus and invest within my circle of competence, both intellectually, in terms of company research and analysis, as well as emotionally in managing my trades and investments.

This all made 2024 a pivotal year for me. Yes, there were mistakes, and I will share my top mistakes, even the most embarrassing ones, with the goal of learning. But overall, there were fewer mistakes, and those I made I realized earlier on and moved to fix, trusting my process.

I’ll use this review to take a look at:

My current portfolio

Major changes vs 2023

Main lessons learned during 2024 and analyzing whether I implemented 2023’s lessons

Before diving in, there is another, quite large, caveat to my positive outlook on 2024. The market performed phenomenally well. With humility and self-doubt, I approach this year in review. It is a well-known human bias to attribute skill to our successes and misfortune to our failures. In investing, I find this to be one of the hardest things to navigate. While I rely on decision-making frameworks, like those by Annie Duke, to evaluate my performance, even with these tools, it remains a challenge to assess how well I’ve done based on my effort and process vs dumb luck - when the entire market is up 30% in a year.

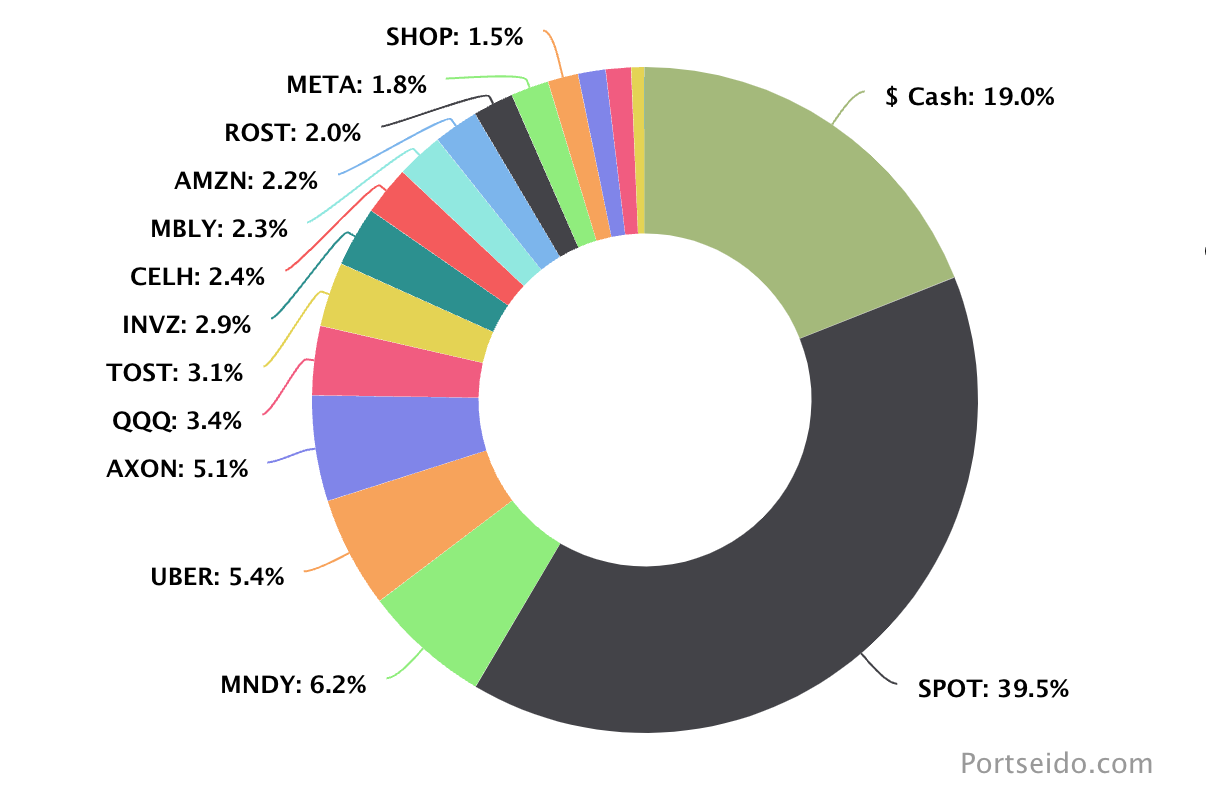

2024 portfolio

My equity portfolio rose 51.85% in 2024, while my crypto holdings rose 48%, for a total portfolio gain of 50.5%. I ended 2024 with 16 positions, down from the 22 I owned in 2023. This narrowing is a positive, as I exited several positions I felt I had no edge in, to instead invest in the QQQ. Over time I hope to decrease the size of my core holdings even further as well as reduce the turnover. This will be dependent on finding true outlier winners.

My 2024 end of year portfolio:

Core positions

Spotify

Spotify is once again my largest position, increasing it’s size in my portfolio by 4%, and drove a lot of the outperformance with a whopping ~140% return for the year. While I tried my hand at trading the ‘top’ earlier in the year, I realized that I’d be far better off simply holding, and so I did, despite the massive run up and lofty valuation.

While I managed to successfully trade a local top in March, all this accounted too was a 4-5% gain on a small portion of my position. After taxes and the headache of monitoring the stock and the added chance of missed opportunity cost where I don’t make the exact right trade, I decided these kinds of trades simply aren’t worthwhile. The odds of me getting all the factors right to properly top tick a great company aren’t high enough to justify.

The far harder part of holding Spotify occurred late in the year following the company’s Q3 report when it soared and reached a market cap of ~$96 billion. Now the question of whether to sell became a major decision for me - both in terms of portfolio management and in terms of the valuation of the company.

The first issue is strictly around portfolio management. Assuming I still believe in the upside of Spotify the company, the question for managing my portfolio going into 2025 is two fold: do I want to take the chance of 40% of my portfolio underperforming due to either a significant pullback in the stock or alternatively, not pulling back but simply not outperforming the market? Spotify has appreciated so much, its odds of beating the market are now shrinking almost by default. How can I afford to not trim and reduce this risk?

The second issue is simply the company’s valuation. At $100 billion, isn’t it fully valued? The second question naturally informs the first issue - if the company isn’t overvalued and I believe the upside is still there, it might be worth holding onto for the next few years. If the company is overvalued, it makes sense to trim or even exit the position.

I agonized over this issue for several weeks as I explored my analysis of the company once more. All of my analysis led me to the conclusion that despite it’s valuation, Spotify is still undervalued, still has significant upside and despite (or perhaps because of) its run up, the company’s future is once again misunderstood by many market talking heads.

Spotify is an incredibly durable business. Users stick around for decades and the willingness to pay increases over time. The questions around valuing the business are:

How many users can they acquire over time?

What will the ARPU be?

What will the margin and operating income or FCF look like?

Based on my answers for these questions, My base case is that if it optimized for operating income, Spotify could be making $7 billion in income within 5 years. Based on its moats and future growth prospects a 25 P/E wouldn’t be out of the ordinary, implying a $139B market cap. While this isn’t a conservative estimate per se, it’s also not overly aggressive, with the amount of levers Spotify has in their business.

While my brain is telling me to trim and reduce my risk on Spotify, one of the lessons I’ve tried to learn over the past few years is that once you find a successful company, with durable growth, moats, future optionality and the management to capitalize on it - just hold on.

Cash and the QQQ

I’ve debated all year long how much cash to be holding. While valuations are lofty, time invested in the market is a critical factor. I decided to maintain a ~10% cash position for most of the year and deploy into the companies I opted to build a core position in over time. Over the summer as the market continued to rise I raised further cash, bringing my cash position to a high of ~20-25%. I'm ending the year with 19% in cash. While that’s quite high, it’s also what helps me sleep at night and provides a measure of anti-fragility to my portfolio.

The QQQ is a position I’ve been looking to add to opportunistically and slowly over time. Especially if I can’t find a more compelling opportunity, which actually didn’t happen all that often this year. After a few buys early in the year to establish a large enough position, I haven’t added to it any more.

Monday, Axon, Toast

My next largest core holdings are Axon, Monday and Toast. All three had fabulous operating years, showing further signs of earnings durability, improved competitive position and future growth. I was opportunistic and patient with each throughout the year, determined to build a position slowly and responsibly. All three are richly valued on traditional metrics and trade in a volatile fashion.

For all three I added on large dips or post earnings when further clarity on the company was received:

Amazon, Meta, Ross Stores and Shopify

Rounding out my core positions, albeit smaller ones, are these old time favorites. I bought back into Meta and increased Amazon earlier this year and believe they’re two of the magnificent seven who have more fundamental upside. Ross stores is my ‘boring’ bet that has kept on delivering for years and adds significant diversification to my portfolio away from its tech based theme. Management is changing and so I’ll be keeping a closer eye on this one going forward to make sure the transition is smooth. Shopify keeps on delivering and growing in an incredible growth space. I’ll be looking to add to Meta and Amazon on pullback while Shopify and Ross Stores are more likely to remain similar size.

Special positions

Uber

Uber has been an ‘invest and investigate’ company for a year now and has recently turned into a full on trade. I shared my thinking here. One of the lessons I learned this year is that for a trade to be worthwhile, it has to be a large enough position, hence when I put on my Uber trade I made it a significant 5% chunk of my portfolio. I’ll be looking to explore Uber further and see how the autonomous driving market evolves. My research will be the determining factor whether Uber turns into an investment and core position or simply a trade.

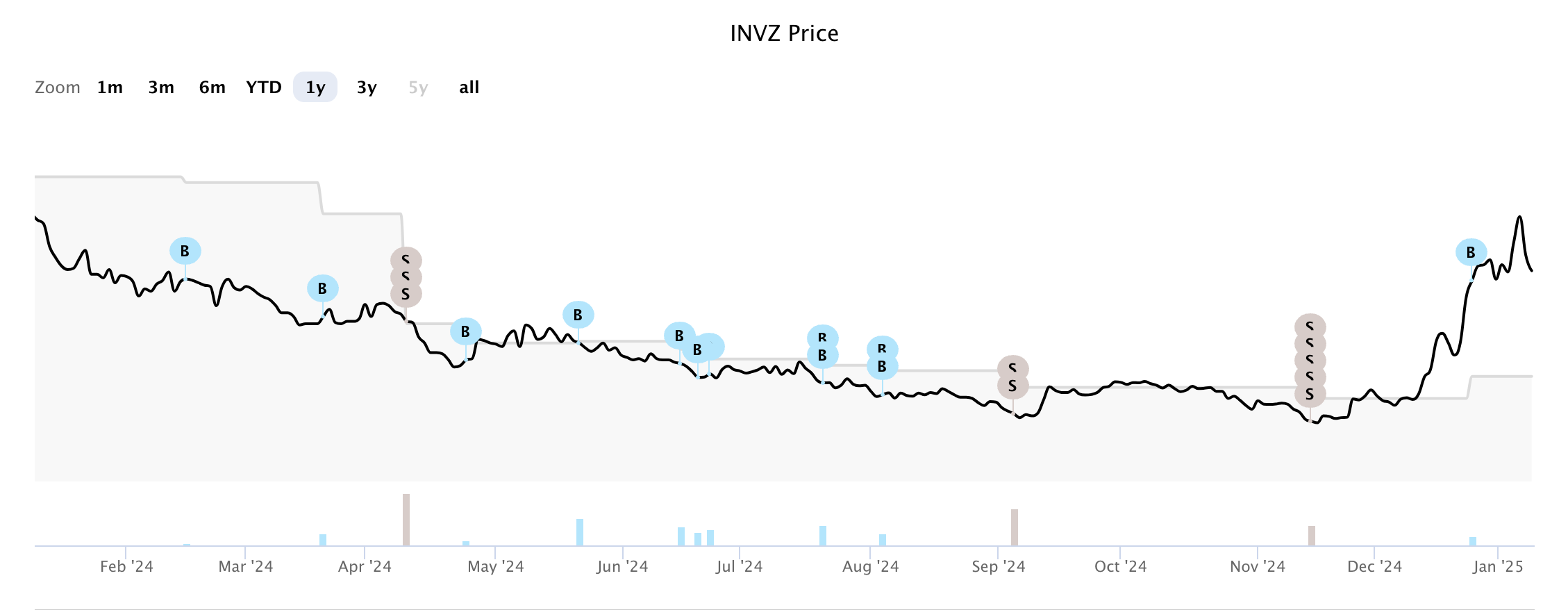

Innoviz

Innoviz is my next ‘big contrarian bet’ and a company I hope can carry the portfolio performance in the latter part of this decade. I’ve recently shared my deep dive into the company (part 1, part 2 and part 3 coming soon). It’s been a wild ride with this one for the past two years and while I’m ending the year up dramatically on it, my Innoviz position receives the ‘worst mistake of the year award’. I’ll elaborate below.

The important development came late in the year for Innoviz, where they closed $80 million in NRE funding over the next few years, $40 million of which is coming in 2025. This greatly alleviates the concerns for the company running out of cash and has broken the company’s death spiral. It was touch and go for a while but I’m much more confident in their prospects going forward and despite the stock rising from a low of ~0.5c to ~$1.5, it’s still a better buy today than it was then. I’ll be looking to add to Innoviz this year and make it a larger position, up to 20% of my portfolio in terms of cost basis, if things go properly. Innoviz trades incredibly sporadically and going up and down 50% happens multiple times a year, so I’ll be very very patient with this one going forward, however the FOMO here is strong.

Celsius and Mobileye

I put these two positions on this year as an aggressive ‘invest and investigate’. Essentially these are both high quality companies, each suffering through a setback. I wanted to monitor both in depth and because they’re both free cash flow generative and I understand their businesses already going in I felt comfortable putting on larger starting positions.

Celsius was a growth market darling that fell from grace and while it’s not a broken company, it’s definitely a broken stock. The big questions regarding Celsius is whether the energy drink market is going to grow again, and at what pace as well as what is Celsius’ moat and competitive position in this highly commoditized and competitive market. Over the past few years they’ve shown their ability to operate on the highest level so I’m fine with watching and giving management a benefit of the doubt, however the next two quarters are going to be key and if they don’t accelerate growth once more to low double digits, this stock could reprice once again.

Mobileye is the leader in ADAS and future autonomous driving solutions and a company I know quite well from my days in the automotive industry. They’re going through a year or two of declining growth due to China woes and a general malaise in the automotive industry. That aside, their future prospects in selling advanced ADAS and autonomous systems are very bright. However, this is a long term story - most of their offerings will only hit the market in 2027 and beyond. Two large overhangs are weighing on the stock: Intel owns 80% of the shares and is likely to be a seller and future competition from lower end solutions. I’m very positive on Mobileye’s ability to win in the autonomous market and believe that the timing is finally right for companies in this space (similar to Innoviz). I’ll be looking to buy on significant pullbacks, but am also concerned with Intel’s position.

2023 vs 2024

2024 saw several significant changes vs 2023. I refined my research process, improved my process in terms of discipline and focused in further on my investment approach which is inspired by Howard Marks’ ‘Fewer losers or more winners?’ and Michael Mauboussin’s expectations investing framework.

Focusing on fewer names

I exited 16 names during the year: HAS, CAVA, ADBE, PANW, SBUX, SNOW, DPZ, HON, AAPL, GOOGL, LOGI, MSFT, MKFG, NKE, DM, TEAM.

Hasbro, Apple, Palo Alto Networks and Nike were trades that I exited, Palo Alto, Apple, and Hasbro as successful trades, Nike as an unsuccessful one, but at least where the process worked.

I exited Markforged and Desktop Metal, my 3D learning positions. They served their purposed and the sector didn’t pan out. The rest of the names were exited because I decided they either didn’t offer enough upside (LOGI) or I simply couldn’t justify them above holding the QQQ. This was part of my learnings from 2023:

Narrowing focus. Closing most positions for the index and betting larger on companies I think can outperform over the next 2 years.

Adobe, CAVA and Starbucks were core positions that I exited. Starbucks and Adobe because of lackluster results. Cava because it simply became too pricey. Two other positions I sold were Microsoft and Google due to high valuations, and a desire to raise cash in the summer.

Trading opportunistically

I made several trades throughout the year: Hasbro, Apple, Palo Alto Networks, Nike and Uber. Most of these were good trades and yet in the grand scheme of things weren’t incredibly impactful to my portfolio’s bottom line. Taking Apple as an example, I bought Apple during drawdowns earlier in the year and sold in July for a 26% overall gain. Yet because of position sizing, this fantastic trade only led to a 50bps outperformance for my portfolio. A similar case occurred in PANW.

I’m aware that in a choppier or more challenging year, trades like this can dramatically improve performance, yet I come away from this year believing that in similar cases in the future, I should aim to make the trading position much larger so as to be meaningful.

What’s a ‘similar situation’? At times, large cap, FCF generating companies sell off dramatically. Sometimes these can be justified, like in the case of Nike, other times - it’s simply a local rebalancing for the company stock. These opportunities, especially in best of breed companies in industries I understand (retail brands I’ve learned is not one of those) are often golden - and it’s why I put my Uber trade on at a 5% position.

Overall I’m happy with my approach to trading opportunistically and will look to continue doing this in 2025.

Mistakes!

My big mistake of the year was with Innoviz, and there were multiple errors here. This embarrassing chart says it all.

What was most embarrassing was that I didn’t make these mistakes for lack of research. No, they were despite the extensive research and thorough knowledge of the company. I simply failed to listen to myself and follow through with my own action plan. If only I'd heeded my own advice, I would have avoided these mistakes.

During my research into Innoviz in 2023, I knew two things about the company. First, they would need to dilute significantly at some point during the first half of 2024. Second, this was a high-risk, long-term play. There was no rush to build a position quickly. I also recognized that 2024 would be a pivotal year for the company.

The first mistake I made was letting FOMO (fear of missing out) get to me at the end of last year and the beginning of 2024, leading me to add to my position early on before the anticipated dilution. This resulted in a slightly oversized position, which I trimmed. You’d think that after letting FOMO get the better of me once, I’d be more disciplined. You’d think.

After the company's capital raise, the stock price dropped precipitously, and I doubled down on the stock throughout the entire summer, not wanting to ‘miss the bottom’. This despite worsening fundamentals over the year. This led to a much larger position in the company than my risk assessment warranted.

During Q3, I recognized these mistakes, and despite the worsening fundamentals and an increased likelihood of the company running out of cash, I decided to own the loss and cut the position from 10% of my portfolio down to the 2% that the fundamentals warranted. To add insult to injury, when I sold during early Q4, I literally sold the bottom and sold at the worst time.

The result is a twofold loss: the loss on the position, and now, with the company's fundamentals dramatically improved, I find myself with a smaller position than I would have liked had I simply followed my original buying plan.

I have three main takeaways from my Innoviz mistakes. First, I need to stick to the process. I have a written buy plan, and I must adhere to it. There's a reason I put it in place, as it is more reliable than buying based on emotional swings.

Second, incredibly small-cap and volatile stocks should have much wider bands for buying, both in terms of price and time. Buying on the way up is better than trying to pick the bottom of a falling knife.

A positive takeaway is that my ability to own the mistake late in the year demonstrated my capacity to ignore my ego and acknowledge my fallacies. While the company has managed to pull itself together and deliver an outstanding 2024, it could have easily gone the other way. In that case, I would have been glad to have cut my loss from a 10% position to a 2% position and salvaged the rest. With clearer eyes and a more disciplined approach, I move forward into 2025.

The second mistake I made in 2024 was a silly oversight, on the one hand but identical in nature to the first mistake. When I sold Google earlier in the year, I wrote:

I am putting in guard rails for when to know whether I've made a mistake and I'll buy back shares in these fabulous companies if:

Price drops 25-40%

Despite having put that into writing, I didn't actually buy. There was no real reason that I didn’t beyond logistics.

Looking back at lessons learned in 2023

When I wrote my 2023 review my main takeaways were:

Hold onto outperforming companies and don’t sell. If a 'big bet' works out, hold on for dear life as long as the thesis is intact. Don't overthink. Don't overtrade. Spotify carried my 2023 portfolio.

Maintain a disciplined process. Make sure each company matches my investment check list, that risk management is in place, that I've done all of the homework thoroughly, set price targets for buying and selling. A disciplined process would have helped me avoid my biggest loss in Curiosity Stream and helped me buy back quality companies I trimmed.

Pay attention to emotions. I sold too much during 2023 due to emotional scarring from the declines in 2022. I also overbought at times from fear of missing out. Maintaining discipline and writing trade and investment processes will help mitigate this.

I’d rate myself as a C on the above three. While I did manage to implement #1 fully, and I improved #2 & #3, there were times as noted above when I didn’t follow my process with the discipline and rigor that I need. While the market was kind enough to provide me with a supportive backdrop for mistakes, I need to do better.

My key lessons from 2024? Very similar:

Adhere to my disciplined process! Continue to write, continue to do deep research and adhere to the process.

Pay attention to emotions. Avoid FOMO as much as possible, be cognizant that we’ve been on a record breaking 2 year streak and investing isn’t that easy.

Position sizing really matters. Make sure that trades are worthwhile and risky positions are sized accordingly.

Looking ahead

Looking ahead at 2025 and 2026 my portfolio has a few areas of opportunity as well as some fragility points.

The first and most obvious one is Spotify. If Spotify underperforms that will hurt my portfolio performance. The second is the risk in the trades I’m making. As part of my lessons from this year, my trades have evolved into larger positions, yet I haven't instituted clear stop losses for these trades. My position sizing in Uber is an example; I put in 5% of my portfolio, but I would be willing to buy another 5% at a much lower price point, around $48, and so there’s quite a large potential for loss on my trades which I’m uncomfortable with.

The third issue is the concentration in high-growth technology companies; anything that impacts this sector will affect my portfolio dramatically.

My response to these issues is zooming out and taking the long term view while holding top notch companies. It’s easy to claim to be a long term holder of great companies, it’s much harder to do in practice. The temptation to be cute and try to rebalance at the right time, trade in and out at seeming market turning events, is quite real.

Yet objectively, most investors struggle to do that well.

I don't think I am different. Therefore holding onto top notch companies, like Spotify or the rest of my high growth portfolio, for the long term is how I choose to deal with these setbacks. It’s important to not lose sight of goals in times like these: over the past two years my portfolio has compounded at ~65%. That is far above and beyond my wildest imagination. Trying to be cute and optimize things sounds like a recipe for failure whereas accepting a year or even two of underperformance in return for staying true to my strategy sounds a much healthier approach.

What am I excited about looking forward?

Without going into the macro or the AI trend, which are both positives, I’m very excited by the final arrival of autonomous vehicles. I’ve been involved in this space since 2015, and the time is finally arriving where products are going to hit the road. This means the time to invest in companies like Innoviz and Mobileye is now, and provides a healthy opportunity going into 2026, 2027 and 2028 for my portfolio. I will be patient and willing to build these positions ahead of this wave.

I’m also excited to improve my process, discipline and keep on buying ownership stakes in wonderful businesses like Axon, Monday, Toast and Amazon.

Here’s to an interesting 2025!

Nice post! Appreciate the thorough explanations. I also have an issue with reducing the number of holdings in my portfolio. I have about 32 now and would like to get it down to 15 max.